I'm an Economist at the World Bank's Research Department (DEC) and Research Associate at the Institute for Fiscal Studies. My research focuses on Taxation and Public Economics.

Founding member of DaTax, the World Bank's new tax data lab.

I did my Ph.D. at UC Berkeley under the supervision of Emmanuel Saez, Alan Auerbach, and Danny Yagan, and received the 2020 National Tax Association’s Outstanding Doctoral Dissertation Award (^_^)

Education:

Ph.D. in Economics from UC Berkeley, 2020.

M.A. and B.S. in Economics from UNLP, Argentina.

PUBLICATIONS

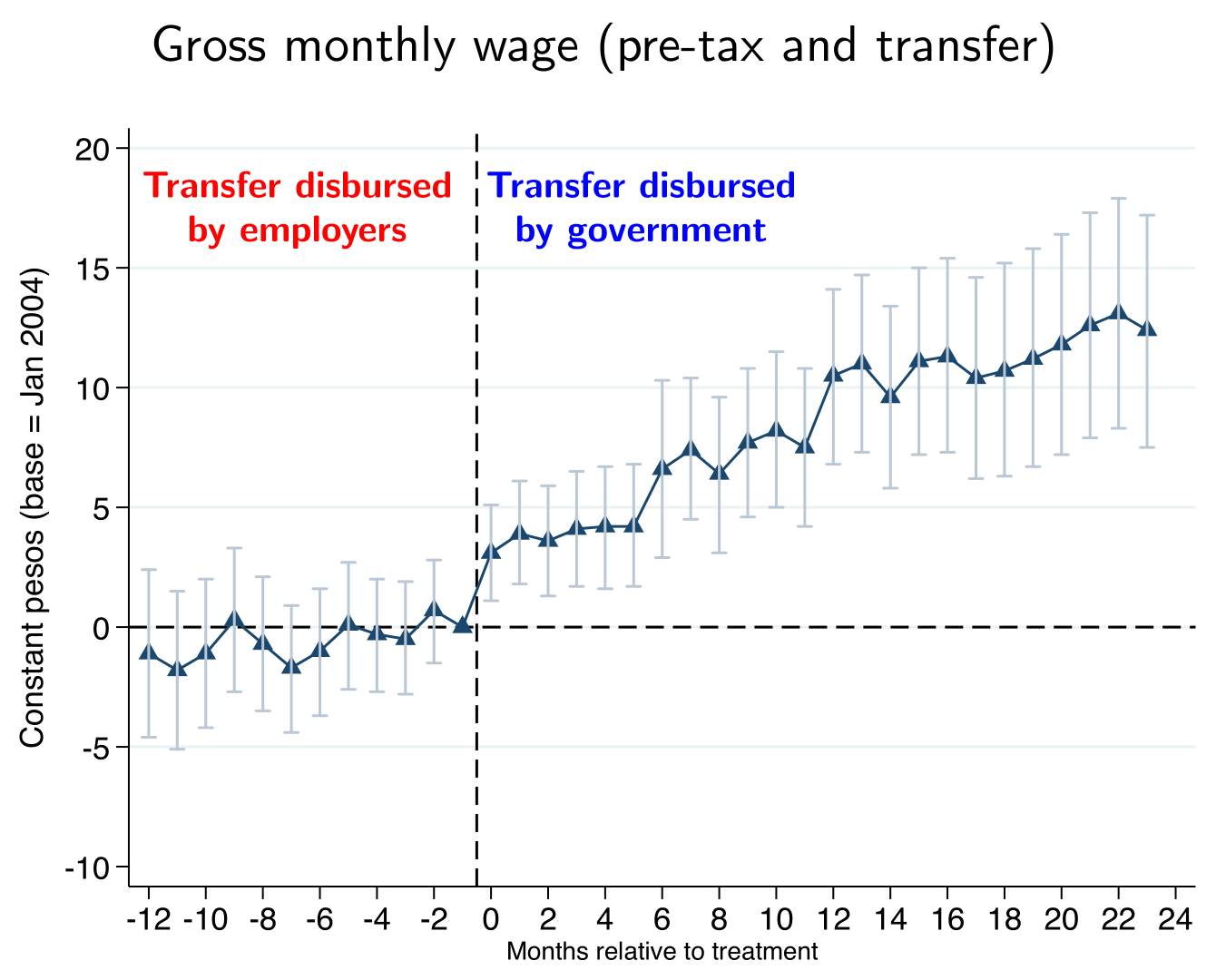

Wage Effects of Means-Tested Transfers: Incidence Implications of Using Firms as Intermediaries

Conditionally accepted at Journal of the European Economic Association

(with Santiago Garriga); Working Papers: [IFS] (Slides)

[ABSTRACT and FIGURE![]() ]

]

ABSTRACT

We show that how countries disburse tax credits matters for economic incidence. We exploit a reform in Argentina that shifted the disbursement of child benefits from employers to the government in a staggered fashion. Using administrative data and an event-study approach, we find that employers receive 5 to 13 percent of the transfers through reduced wages when they mediate the payments. This wage effect is more pronounced for low-income workers, particularly new hires, and in smaller and less unionized firms. We argue that workers likely misperceived firm-disbursed transfers as part of their work compensation, leading to incidence-sharing effects. Our findings suggest that relying on firms as intermediaries in the tax-benefit system can have unexpected labor market consequences.

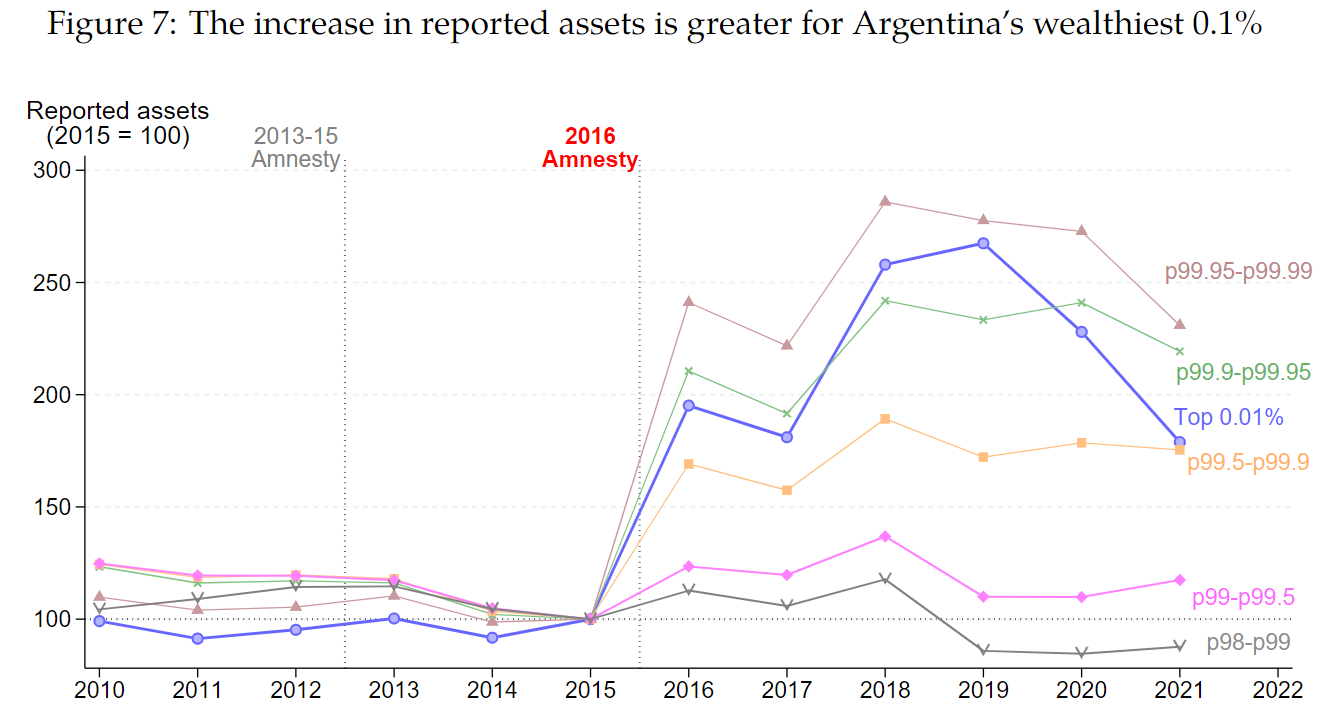

Revealing 21% of GDP in Hidden Assets: Evidence from Argentina

Journal of Public Economics, October 2025, 250: 105471.

(with J. Londoño-Vélez); [Gated version]; Working Papers: [UNU-WIDER] [EU Tax Obs] [World Bank] (Slides)

[ABSTRACT and FIGURE![]() ]

]

ABSTRACT

Argentina’s 2016 tax amnesty led to the disclosure of hidden assets totaling 21% of GDP—an exceptionally large amount, concentrated offshore and among the wealthiest 0.1%. We examine how this enforcement initiative affected taxpayer behavior, tax progressivity, and revenue. Compliance improved—especially among high-wealth individuals—expanding the bases of both the wealth and capital income taxes. A subsequent tax hike on foreign assets further enhanced progressivity and raised effective tax rates on the top 0.1%, generating nearly 0.8% of GDP in wealth tax revenue—one of the highest yields globally. We discuss why, despite prior failed amnesties, Argentina’s 2016 policy package proved unusually effective.

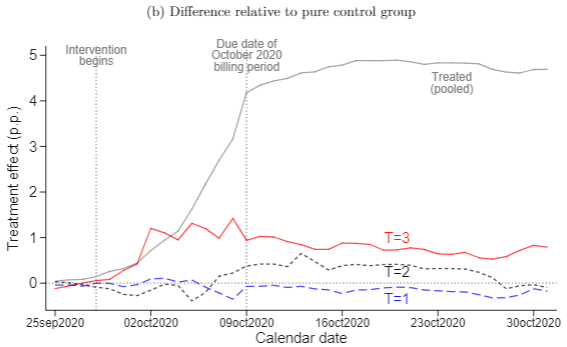

Design of Partial Population Experiments with an Application to Spillovers in Tax Compliance

The Review of Economics and Statistics, January 2025, 1-45.

(with G. Cruces, G. Vazquez-Bare); [Gated version] [IFS WP version] (Slides long) (Slides short)

[ABSTRACT and FIGURE![]() ]

]

ABSTRACT

We develop a framework to analyze partial population experiments, a generalization of the cluster experimental design where clusters are assigned to different treatment intensities. Our framework addresses cluster heterogeneity, which is pervasive in empirical settings but commonly ignored when designing experiments. We consider two sources of heterogeneity: heterogeneity in cluster sizes and heterogeneity in outcome distributions across clusters. We study the large-sample behavior of OLS estimators and their corresponding cluster-robust variance estimators and show that (i) ignoring heterogeneity in experimental design may result in severely underpowered experiments and (ii) the cluster-robust variance estimator may be upward-biased when clusters are heterogeneous. We use our results to derive formulas for power, minimum detectable effects, and optimal cluster assignment probabilities. All our results apply to cluster experiments, which are a particular case of our framework. We set up a potential outcomes framework to interpret the OLS estimands as causal effects. We implement our methods in a large-scale experiment to estimate the direct and spillover effects of a communication campaign on property tax compliance. We find an increase in tax compliance among individuals directly targeted with our mailing, as well as compliance spillovers on untreated individuals in clusters with a high proportion of treated taxpayers.

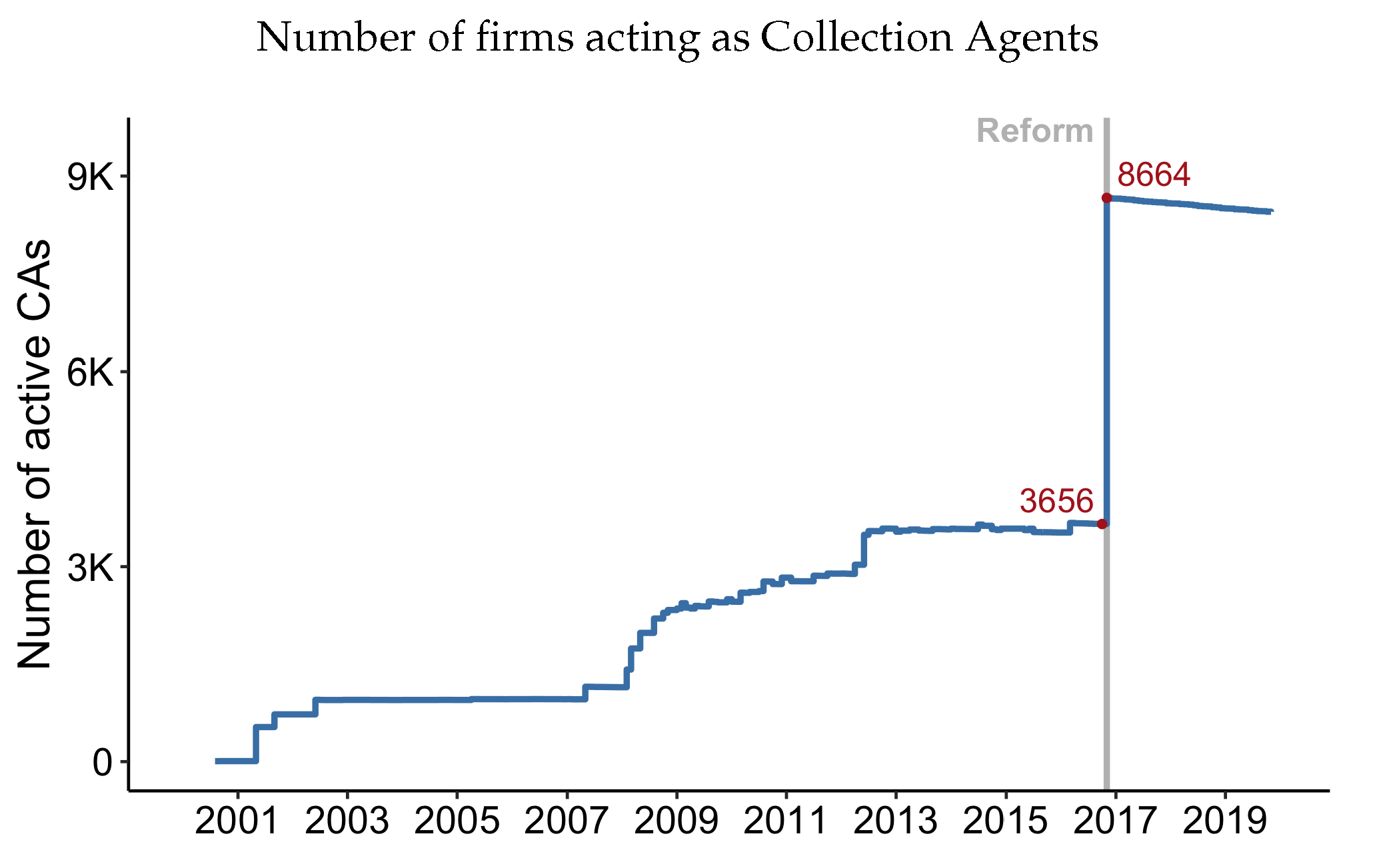

Firms as Tax Collectors

Journal of Public Economics, May 2024, 233: 105092.

(with P. Garriga) [Gated version] [IFS Working Paper] (Slides) Summary for a broader audience: WB Development Impact Blog

[ABSTRACT and FIGURE![]() ]

]

ABSTRACT

We show that delegating tax collection duties to large firms can bolster tax capacity in weak-enforcement settings. We exploit two reforms in Argentina that dramatically expanded and subsequently reduced turnover tax withholding by firms. Combining firm-to-firm data with regression discontinuity and difference-in-differences methods centered on revenue eligibility thresholds, we find that: (i) appointing large firms as collection agents (CAs) does not hinder their economic activity, (ii) it leads to a significant increase in self-reported sales and tax payments among CAs' business partners, (iii) these effects are primarily concentrated among downstream firms that lack a traceable paper trail, and (iv) reductions in withholding lead to a decrease in self-reported sales, albeit to a lesser extent. Tax-collecting firms can thus help boost tax compliance and revenue.

Oxford Review of Economic Policy, Autumn 2023, 39 (3): 530-549.

(with M. Bérgolo and J. Londoño-Vélez) (Gated version) (Slides)

WORKING PAPERS

Revise & Resubmit at American Economic Review

(with Youssef Benzarti and Santiago Garriga). (Slides) Working Papers: [NBER-WP]

Presentations: University of Oxford, University of Michigan (Ford), World Bank, Imperial College London, KOF-ETH Zurich, 9th Mannheim Taxation Conference, MAP Seminar Peru, UdeSa Argentina, IECON-UdelaR Uruguay, University of Oslo, NBER Public Economics, Fall 2023, 80th IIPF Annual Congress

Summary for a broader audience: FocoEcónomico, WB Data Blog

ABSTRACT

We estimate the effect of a temporary VAT cut and its re-introduction, along with antiprofiteering measures, on food necessities during a period of high inflation in Argentina. Using barcode-level data from over 3,000 supermarkets, we find that: (1) without anti-profiteering measures, prices rose more after the VAT was reinstated than they fell after the cut, with this asymmetry persisting over time; and (2) anti-profiteering measures curbed price increases following the VAT hike. A welfare model shows that the VAT cut had progressive effects and that anti-profiteering measures mitigated the regressive impact of asymmetric pass-through.

Reject & Resubmit at Journal of Political Economy

(with Nicolas Ajzenman, Guillermo Cruces, Ricardo Perez-Truglia, and Gonzalo Vazquez-Bare) Working Papers: [NBER]

Summary for a broader audience: VoxEU-CEPR

ABSTRACT

This paper investigates the relationship between tax progressivity and compliance. We leverage a major progressive tax reform in a large Argentine municipality. First, we use a quasi-experimental design to estimate the causal effect of changes in a household’s own tax rates on its tax compliance. Second, we utilize a large-scale natural field experiment to examine whether, holding a household’s own tax rates constant, tax compliance is influenced by the tax rates of poor or rich households. We find that reducing taxes for poor households increases their compliance, while increasing taxes for rich households decreases theirs. When poor households learn about the tax hike on the rich, this increases their stated perceived fairness of the tax system and their actual tax compliance. When rich households learn about the tax cuts for the poor, their stated perceived fairness also increases significantly, but their compliance, if anything, goes down. Leveraging a further reform and an additional field experiment that took place a year later, we show that both the quasi-experimental and experimental findings replicate. Our evidence highlights that tax compliance depends not only on a household’s own tax rate but also on how they truly feel about the broader tax schedule. Our findings also highlight the gap between stated and revealed preferences for redistribution. Lastly, we conduct a counterfactual analysis to illustrate the implications of our findings for the design of tax policies.

(with T. Flores, G. Cruces, J. Bermudez, T. Scot, J. Schiavoni) Working Papers: [World Bank PRWP]

Summary for a broader audience: WB Let's Talk Development

ABSTRACT

This paper investigates gender disparities in residential property ownership and tax compliance in a large Argentine municipality using detailed tax administrative data. While ownership is evenly distributed between women, men, and co-owned properties up to the 40th percentile of the value distribution, higher-value properties exhibit significant gender disparities, with women’s share dropping to less than 20% in the top 1%. Tax compliance increases with property value, with an average evasion rate of 46%, and men and women are equally likely to meet their tax obligations across the distribution. However, women face slightly higher effective tax rates due to owning lower-value properties, which are disproportionately affected by a mildly regressive tax schedule. Gender responses to enforcement measures are also comparable. A soft randomized communication campaign significantly increased timely payments equally for both men and women, with men responding more quickly. Similarly, the findings show no gender-based differences in responses to macroeconomic shocks such as COVID-19. The study underscores the role of property tax in promoting equitable revenue mobilization and highlights the importance of gender-disaggregated data for informing tax policy and enforcement strategies.

(with Guillermo Cruces and Victoria Castillo); (Slides)

Presentations: 2nd World Bank Tax Conference, 53a JIFP (Cordoba), 76th IIPF (Iceland), 8th UDEP Workshop (Peru), Applied Micro Seminar (UC Santa Barbara), NTA (Tampa), PF Seminar (Berkeley), 13th ACLEC (UC Santa Cruz), Labor Symposium (Berkeley), 18th IZA-SOLE, AAEP meeting (La Plata), RIDGE PF Workshop (Uruguay), NTA (Philadelphia), Ministry of Labor (Argentina), 2nd Zurich PF Conference (U. of Zurich), UNU-WIDER PF Conference (Mozambique)

ABSTRACT

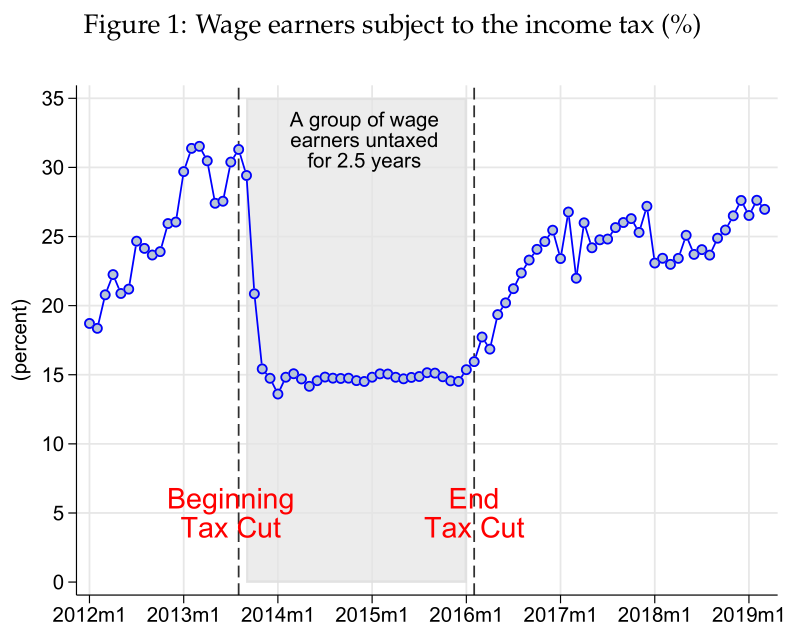

We exploit a large, quasi-randomized, 2.5-year-long income tax holiday to identify intertemporal labor responses of high-wage earners to net wage changes. In August 2013, the Argentine government exempted a group of wage earners from the income tax for 2.5 years while leaving in place the tax on other high-wage earners. Eligibility was based on whether past wage earnings were below a fixed threshold, thus levying sharply different marginal and average tax rates—effectively 0% for workers below the threshold. Using rich population-wide administrative data and a regression discontinuity design, we estimate a precise and very small wage earnings elasticity of 0.017 for this large, salient, and temporary income tax change. Responses are larger for more flexible outcomes (overtime hours) and for more elastic groups (job switchers and managers). We also find avoidance responses from new entrants who faced no tax if their first monthly wage was below the fixed threshold. This strategic entry below the threshold to dodge taxes required coordination with employers. Our findings suggest the presence of rigidities in the labor market, which imply that wage earners' responses to tax changes depend largely on substantial coordination with employers.

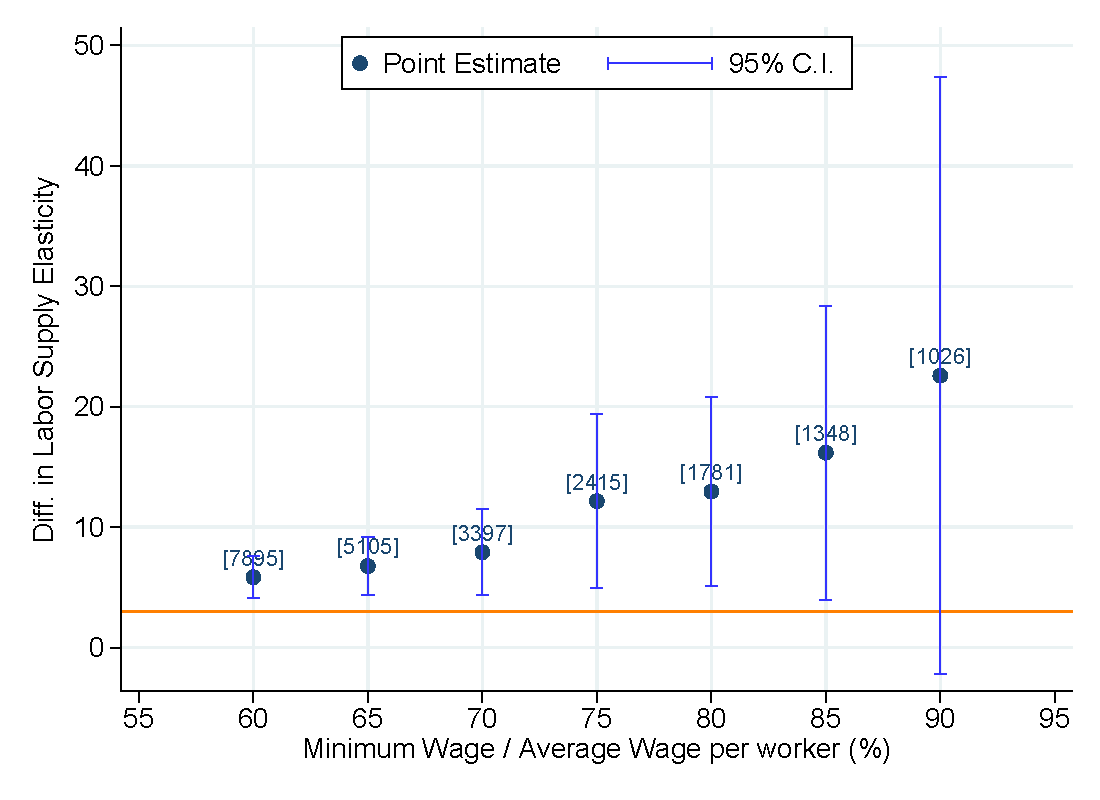

(with Roman D. Zarate) (Slides)

Presentations: SEA 90th Annual Meeting, Labor Seminar at UC Berkeley, Trade Seminar at UC Berkeley, CAF Symposium

ABSTRACT

We disentangle the extent of imperfect competition in product and labor markets using plant-level data. We derive a formula for the ratio between markups and markdowns assuming cost-minimizing firms that face upward-sloping labor supply and downward-sloping product demand curves. We then separate this combined measure of market power by estimating firm-level labor supply elasticities instrumenting wages with a different set of instruments including the use of intermediate inputs, input price shocks, and TFP shocks. Our results suggest that both markets exhibit imperfect competition, but the variation is mainly driven by markups. We also estimate the relative gains of removing market power dispersion on allocative efficiency, finding that markups are more important on TFP than markdowns.

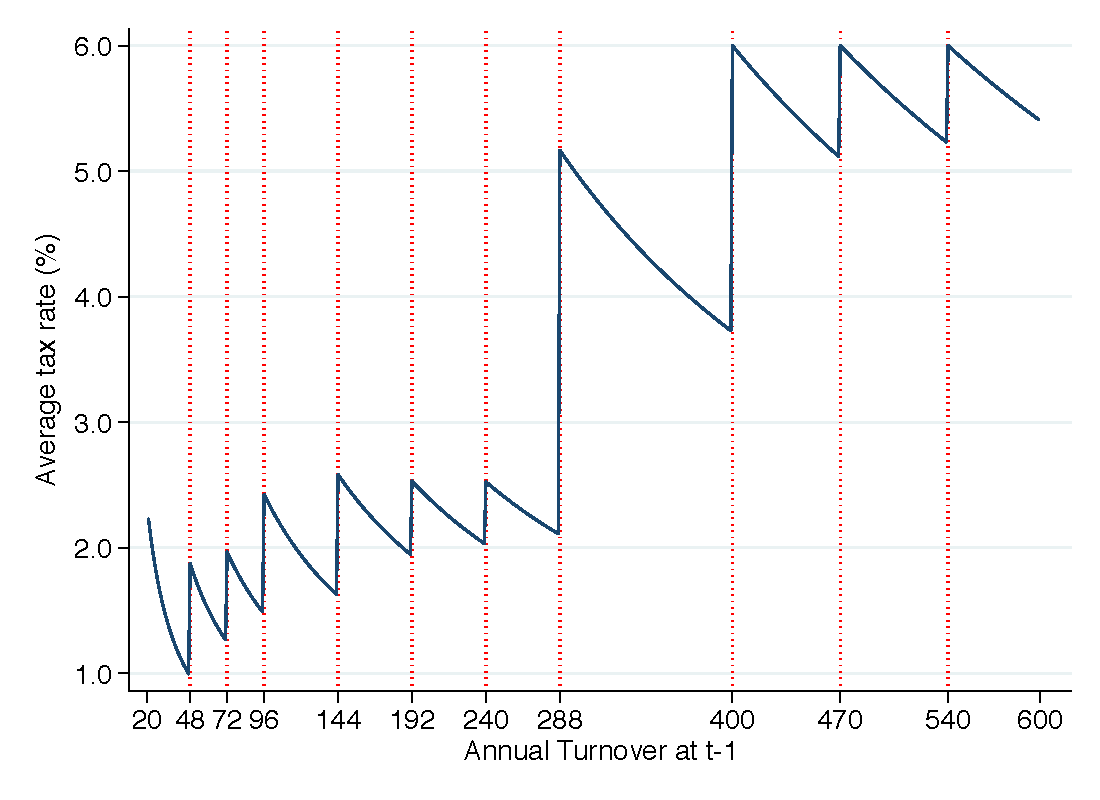

(with Santiago Garriga and Jorge Puig); Revision in progress

ABSTRACT

We estimate the response of firms and self-employed workers to two revenue taxes—Monotributo and Gross Receipts Tax—across the turnover distribution using rich administrative data from Argentina. We exploit several revenue-dependent discontinuities that provide incentives to underreport taxable income combined with a bunching design to estimate sales elasticities. We also explore heterogeneities by firm size, type of activities, and type of taxpayers. In the case of small firms, we find sizeable bunching below the thresholds that is stronger for higher tax incentives. The response is stronger in sectors that have more space for manipulation, such as service-based activities. In the case of medium and large firms, bunching is more muted but it suggests that even large firms are able to underreport their gross sales to avoid facing higher tax rates. Firms also seem to find more costly the indirect administrative cost of becoming a collection agent than the direct fiscal cost of the Gross Receipts Tax. We cannot rule out, however, that large firms adjust other margins (or taxes) to compensate for the higher tax pressure.

SELECTED WORK IN PROGRESS

(with Youssef Benzarti and Santiago Garriga)

Draft will be posted soon

Mobile money represents one of the most transformative advances in communication and financial technology of the current millennium, enabling money transfers through simple mobile text messages. Its diffusion has been particularly impactful in African countries, where access to traditional banking services remains limited. Using billions of mobile money transactions from Tanzania—one of the largest mobile money markets—we document usage patterns across several dimensions, including time of day, day of the week, user loyalty, and gender differences. We further provide novel evidence on behavioral responses to the introduction and subsequent reduction of a levy on mobile money transactions. The asymmetric response we document—characterized by large adjustments along both the extensive and intensive margins following the tax increase, and comparatively muted responses to the subsequent tax decrease—raises concerns about the efficiency costs of this tax. In particular, the common presumption among policymakers that it is possible to overshoot tax rates and later reverse course without lasting effects may not hold, resulting in persistently suboptimal allocations.

(with N. Barahona, Y. Benzarti, B. Diaz de Astarloa, S. Garriga, E. Garcia-Lembergman, and D. Jiménez-Hernández)

Draft will be posted soon

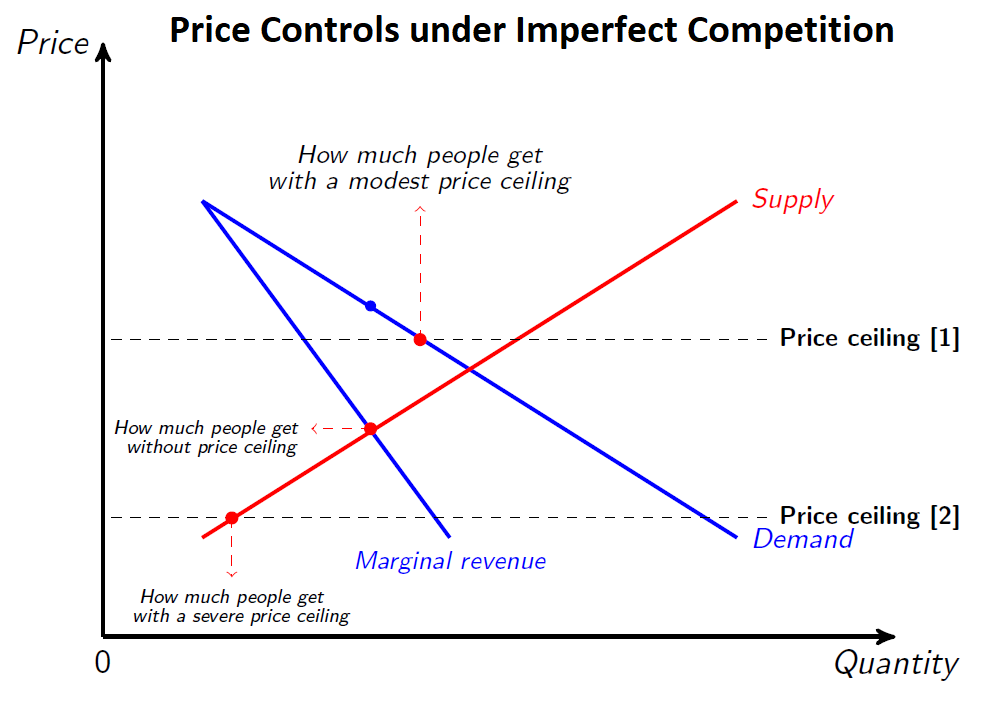

We use scanner data from Argentina to study the Precios Cuidados program, a voluntary initiative in which the government negotiated retail price ceilings with manufacturers in exchange for preferential shelf space and visibility in supermarkets. Using a staggered difference-in-differences design, we find that the program lowered relative prices and increased sold quantities of participating products compared to similar non-participating goods, without causing stockouts. The timing and magnitude of quantity responses suggest that the program increased demand beyond price effects. To interpret these findings and quantify their welfare implications, we estimate a model of firm pricing and consumer demand, where firms voluntarily accept price ceilings that limit their markups in exchange for advertising benefits. Our analysis shows that price control programs may increase consumer welfare by lowering the relative prices of regulated products and their substitutes while providing incentives for firms to voluntarily participate in them.

(with Y. Benzarti, B. Diaz de Astarloa, S. Garriga, and E. Garcia-Lembergman); In progress (Slides)

We use high-frequency scanner data along with several hundreds naturally occurring variation in price controls at the barcode level in Argentine supermarkets, to uncover new facts about price controls in a setting of high inflation. We use an event study approach where treated goods (barcodes) are compared to otherwise similar goods. First, we show that price controls are indeed effective at holding prices fixed and observe a high rate of compliance. Second, we find little evidence of wide-spread shortages due to the introduction of price controls. Instead, we observe a large increase in quantities purchased, which double on average, as price controls keep prices lower relative to other goods. Third, prices revert to slightly higher levels once a given barcode is no longer subject to price controls, suggesting that such interventions do not have any long lived effects on inflation. As a result, quantities purchased of the controlled barcodes decrease. We also explore substitution behavior between products subject to price controls and close substitutes. The policy seems to have no distributional effects since it benefits rich and poor households equally.

We study to what extent the implementation of evaluation laws affects reported tax expenditures. We exploit the staggered introduction of tax incentives evaluation laws (TIELs) in US states, from 1999 to 2019. Using a novel digitized database of states’ tax expenditures and an event study approach based on the year these laws were enacted, we show that evaluation laws matter for transparency. We find that following the implementation of TIELs, reported tax expenditures increased on average by 14%, equivalent to about 2.44 billion USD at 2023 prices. This effect persists even four years after the laws are introduced. However, we find no changes in states’ tax revenues and direct spending after the TIELs were passed, which indicates that the observed higher reported tax expenditures correspond to previously hidden undisclosed tax expenditures provisions.

POLICY PAPERS

Anatomía del Impuesto a las Ganancias sobre los Asalariados: Argentina 2000-2016

In preparation for Revista de Trabajo (Ministry of Labor, Argentina)

Investment in ICT, Productivity, and Labor Demand (SSRN WP) (Updated version)

(with Irene Brambilla), World Bank Policy Research Working Paper No. 8325 (January 2018)

Pre-doctoral![]()

Growth in Labor Earnings Across the Income Distribution: Latin America During the 2000s

(with Irene Brambilla), CEDLAS, Working Papers 182, CEDLAS, Universidad Nacional de La Plata, 2015.

An Empirical Analysis of Mark-ups in the Argentine Manufacturing Sector

(with Irene Brambilla), Department of Economics, Working Papers 104, Departamento de Economía, Universidad Nacional de La Plata, 2014.

Female Labor Supply and Fertility. Causal Evidence for Latin America

CEDLAS, Working Papers 0166, Universidad Nacional de La Plata, 2013.

Measuring Poverty in Argentina: the Food Energy Intake Method

(with Malena Arcidiácono), XLVII Annual Meeting of the Argentine Association of Political Economy, 2012.

Other Publications

Fiscal Decentralization and Economic Integration in Mercosur: Argentina and Brazil

(with Alberto Porto, Natalia Porto), Latin American Business Review, 15:3-4, 225-252, DOI: 10.1080/10978526.2014.931787

"Glocalization" and decentralization. The role of local governments in the new international context

(with Alberto Porto, Natalia Porto), Urban Public Economics Review, num. 20, pp. 62-93.

Chapters in books

La Calidad de la Administración Tributaria como Insumo de la Función de Producción Recaudatoria

(with A. Porto and W. Rosales), In Porto A. (editor), Temas de Economía de los Gobiernos Municipales, Buenos Aires: Ed. DUNKEN. 2012. ISBN: 978-987-02-6003-5.

★ A Primer for Doing Tax Research with Administrative Data [Slides]

Public Economics: Taxation (MSc in Economics, UNLP) --- [SEE CONTENT![]() ]

]

Economía Pública: Impuestos (2025)

Esta pagina contiene los materiales del medio-curso Economía Pública: Impuestos para estudiantes de la Maestría en Economía de la Universidad Nacional de La Plata (UNLP). El curso cubre temas como estructura y diseño óptimo de impuestos sobre la renta y transferencias de dinero, comportamiento de las personas (decisiones laborales, elusión y evasión), modelos de evasión, e incidencia económica. El curso combina teoría y evidencia empírica sobre temas de política actual, como las reformas fiscales y los programas de transferencia utilizando varios métodos econométricos.

Programa: pdf

Lectures

Repaso: Basic theory tools (ver solos)

Quiz: (link)

Clase 1: Intro to Public Economics and Overview of ARG Income Tax-Transfers

Clase 2: Optimal Labor Income Taxation

Clase 3: Optimal Design of Transfers

Clase 4: Labor Supply and Taxable Income Responses to Taxes and Transfers

Bunching

Clase 5: Tax Enforcement

Aplicación: Impuestos sobre la propiedad

Clase 6: Tax Incidence

Quiz: (link)

Bonus lecture: Doing Tax Research with Admin Data

Assignments

Exam: TDB.

Advanced Public Economics --- [SEE CONTENT![]() ] --- Teaching Award 2022/23

] --- Teaching Award 2022/23

Advanced Public Economics -- Fall'22

This page contains course materials for Advanced Public Economics for year-3 undergrads. The course covers topics such as tax and welfare policy, income taxation, social security programs, tax enforcement, tax incidence, and public goods. The course combines theory along with empirical research on current policy issues such as inequality and poverty, tax reforms, and cash transfer programs using various econometric methods.

Syllabus: pdf

Lectures

Week 1: Introduction to Public Economics

Week 2: Inequality, Poverty, Taxes and Transfers

Week 3: Overview of the UK Tax and Benefit System

Week 4: Optimal Labour Income Taxation

Week 5: Optimal Design of Transfers

Week 6: Labor Supply Responses to Taxes and Transfers

Week 7: Taxable Income Responses to Taxation

Week 8: Tax Enforcement

Week 9: Tax Incidence

Week 10: Public Goods

Bonus lecture: How to do Tax Research with Admin Data

Assignments

Problem Set 1 /// (Solutions)

Problem Set 2 /// (Solutions)

Problem Set 3 /// (Solutions)

Final Exam /// (Solutions)

Teaching Evaluation from Students /// (scores)

Teaching Award /// (certificate)

Evaluación de Políticas Públicas (in Spanish)--- [VER CONTENIDO![]() ]

]

Política Pública en Acción: Analisis y Evaluación de Políticas Públicas -- Julio 2022

En este curso se realiza una revisión general de herramientas econométricas utilizadas en la evaluación de políticas públicas (clases en Zoom) y se discuten aplicaciones de papers recientes que buscan estimar el impacto causal de diferentes políticas (clases presenciales).

Programa: pdf

Clases

Slides 1: Contrafactuales, Analisis de Regresion, Matching

Slides 2: Asignacion Aleatoria, Variables Instrumentales

Slides 3: Diseno de Regresion Discontinua

Slides 4: Diff-in-Diff, Event Studies, Control Sintetico

Slides 5: Aplicaciones de Asignacion Aleatoria

====> Ejemplo Randomizacion en Excel

Slides 6: Aplicaciones de RDD

Slides 7: Aplicaciones de Diff-in-Diff y Control Sintetico

Ejercicios y Consigna Final

Ejercicio 1

Ejercicio 2

Ejercicio 3

Trabajo Final

Economic Policy Analysis --- [SEE CONTENT![]() ]

]

Economic Policy Analysis II -- Spring'22

This page contains course materials for Economic Policy Analysis II co-taught with Bouwe Dijkstra. My part of the course focuses on optimal income tax and transfer theory and the empirical literature that estimates behavioural responses to progressive tax systems.

Syllabus: pdf

Lectures

Slides 1: Introduction and Overview of the UK system

Slides 2: Optimal Income Tax and Transfers

Slides 3: Labor Supply Responses to Taxes and Transfers

Slides 4: Taxable Income Responses to Taxation

Assignments

Problem Set /// (Solutions)

Mock Exam

Final Exam

Public Economics 131 (Prof. Emmanuel Saez), Spring 2017 --- [SEE CONTENT![]() ]

]

ECON 131: Public Economics (Spring'17)

This page contains section notes and other course materials

for ECON 131: Public Economics taught by Emmanuel Saez.

Office hours: Fridays 3-6pm, 630 Evans Hall

Section notes

Section 1: Optimization Review -Updated 2017- /// (Solutions)

Section 2: Empirical Tools -Updated 2017- /// (Solutions)

Section 3: Tax Incidence and Efficiency Costs -Updated 2017- /// (Solutions)

Section 4: Labor Income Taxation -Updated 2017- /// (Solutions)

Section 5: Labor Income Taxation (cont.) -Updated 2017- /// (Solutions)

Section 6: Capital Income and Savings Taxation -Updated 2017- /// (Solutions)

Section 7: Externalities -Updated 2017- /// (Solutions)

Section 8: Public Goods -Updated 2017- /// (Solutions)

Section 9: Voting, Tiebout Model, and Local Public Finance -Updated 2017- /// (Solutions)

Section 10: Social Security and Insurance -Updated 2017- /// (Solutions)

Section 11: Moral Hazard and Social Security -Updated 2017- /// (Solutions)

Assignments

Problem Set 1 /// (Solutions)

Problem Set 2 /// (Solutions)

Problem Set 3 /// (Solutions)

Problem Set 4 /// (Solutions)

Additional Practice [optional] /// (Solutions)

Econometrics 140, Spring-Fall 2016 --- Syllabus

Microeconomics 100A, Fall 2015 --- Syllabus

Labor Economics, Spring 2013 (graduate)

Topics in Advanced Econometrics, Fall 2012 (graduate)

Microeconomics II, 2012-2014 (undergraduate)

Econometrics I, Fall-Spring 2011 (undergraduate)

2026

Seminars and Conferences

* UVA Development Econ Seminar, University of Virginia (January 27)

2025

Seminars and Conferences

* BREAD Conference on Development, Princeton (May 2-3) (Program)

* Universidad Nacional del Nordeste, Chaco Argentina (July 2)

* 11th ECINEQ Conference, Washington DC (July 9-11)

* 81th IIPF Annual Congress, Nairobi Kenya (August 20-22)

* 118th NTA Annual Conference on Taxation, Boston (November 6-8)

Policy Talks

* Policy Research Talk (July 4-5) (Slides and recording)

* Prosperity MENA Learning Event (taxation in Algeria) (May 22)

2024

Conferences

* IFS Post-doc Alumni Workshop (July 4-5)

* 80th IIPF Annual Congress, Prague Czech Republic (August 21-23)

* 117th NTA Annual Conference on Taxation, Detroit (November 14-16)

Seminars

* George Washington University (February 26)

* World Bank, MTI-LAC (February 1)

* World Bank, DEC half-baked seminar (April 4)

* Estonian Embassy (April 18)

* World Bank, DaTax launch event (September 24) (Program and recording)

* International Chamber of Commerce, Bolivia (October 8)

2023

Conferences

* EUTO-IEB Workshop on the Economics of Taxation, Barcelona (May 31)

* UNU-WIDER Development Conference, Oslo (September 6-8)

* NBER Public Economics Program Meeting, Fall 2023 (October 19-20)

Seminars

* São Paulo School of Economics (February 27)

* Paris School of Economics, EU Tax Observatory (March 10)

* Oxford University, Centre for Business Tax seminar (March 13)

* Skatteforsk - Centre for Tax Research, Norway (May 10)

* University of Oslo, Econ Department seminar (May 11)

* Universitat de Barcelona, IEB seminar (TBD)

* Servicio de Administracion de Rentas (SAR), Honduras (September 29)

2022

Conferences

* 78th IIPF Annual Congress, Linz Austria (August 10-12)

* 9th Annual Mannheim Taxation Conference, Germany (September 8-9)

* 4th World Bank Tax Conference on Global Tax Equity (September 22-23)

* NBER Public Economics Program Meeting, Fall 2022 (October 27-28)

* 115th NTA Annual Conference on Taxation, Miami U.S. (November 10-12)

Seminars

* London School of Economics, Management (March 3)

* KOF Research Seminar, ETH Zurich (May 11)

* Seminario MAP, Perú (May 16)

* Seminario IECON-UdelaR, Uruguay (June 21)

* Universidad de San Andres, Argentina (July 12)

* Imperial College London, Economics (October 18)

* University of Tübingen (November 29)

2021

Conferences

* NTA 114th Annual Conference on Taxation (paper presented by coauthor)

* 6th Zurich Conference on Public Finance in Developing Countries (2 papers presented by coauthors)

* NBER Business Taxation in a Federal System (paper presented by coauthor)

* RIDGE Workshop on Public Economics

* North American Summer Meeting of the Econometric Society (NASMES)

* CESifo Area Conference on Public Economics 2021

* AEA-ASSA Annual Meeting

Seminars

* IFS-UCL-LSE/STICERD Development Economics Work In Progress Seminar Series

* IFS Work In Progress Seminar

* International Online Public Finance Seminar Series (organized by K. Bilicka and E. Ohrn)

* ZEW – Leibniz Centre for European Economic Research, ZEW Research Seminar

* Next Generation Economics network, NGE seminar series

* Universidad de Guadalajara (CUCEA), Seminario de Investigación Económica